The affordability crisis is a single structural failure expressed across housing, healthcare, wages, public finance, and democratic participation.

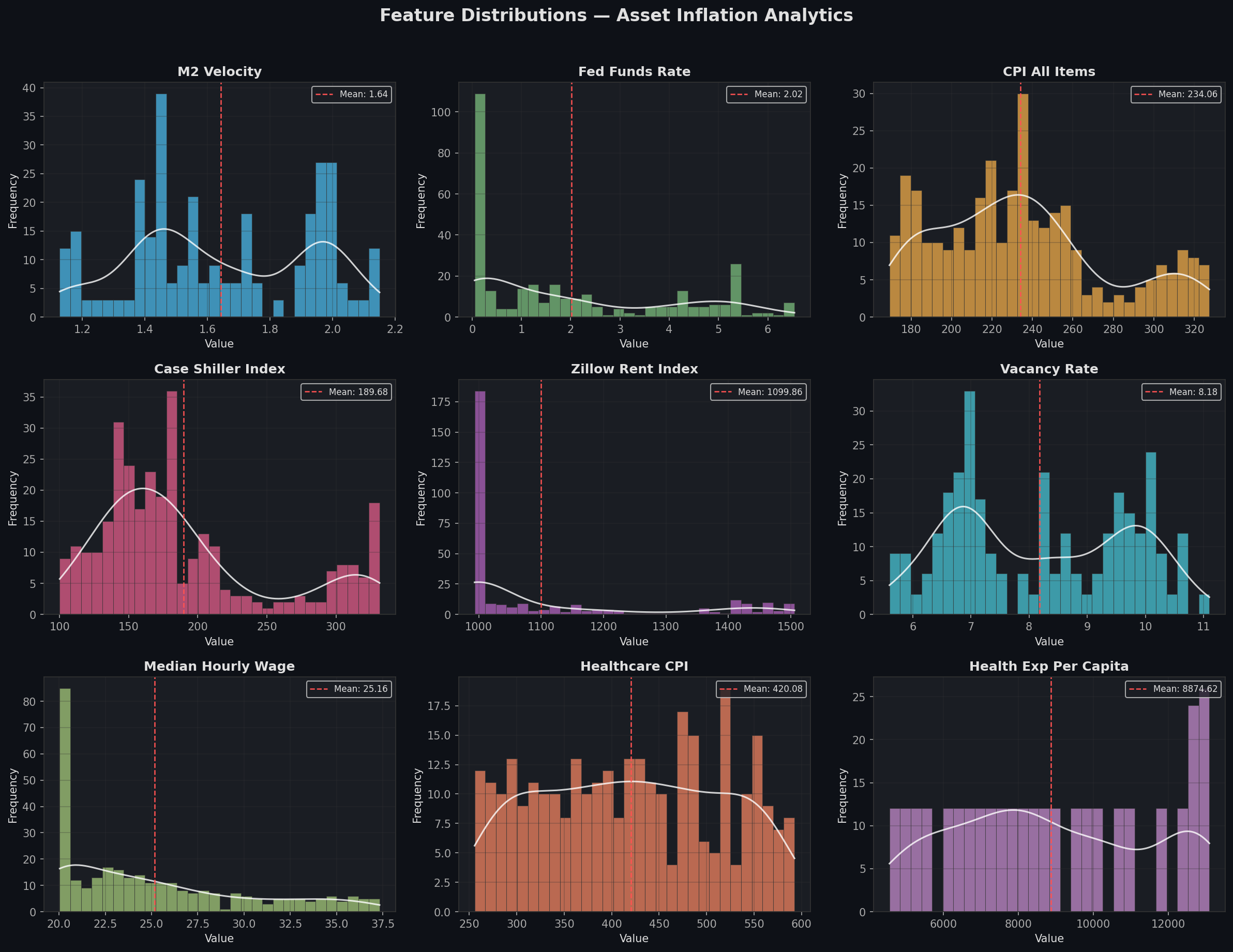

Since 2000, U.S. home prices have risen 227% while wages have risen 86%. The M2 velocity index collapsed from 2.1 to 1.1, meaning each dollar now circulates through the labor economy roughly half as often as it did a generation ago. Money is not flowing through wages. It is pooling in assets. Piketty (2014) formalized this as the condition where the rate of return on capital exceeds the rate of economic growth (r > g), producing wealth concentration as a structural feature of the system rather than a temporary distortion.

The consequences extend beyond the housing market. Government net financial worth fell from -38% to -95% of GDP over the same period (OECD, 2024), reflecting a public sector that borrowed to maintain services while its tax base migrated into lightly taxed asset classes. The IMF's 2018 Fiscal Monitor documented this pattern across advanced economies, noting that governments were "asset rich but getting poorer" as public holdings were sold or leveraged while obligations grew.

The political response has been withdrawal. Solt (2008) demonstrated across 23 democracies that rising economic inequality depresses voter turnout, with the strongest effects concentrated among lower-income citizens. Gilens and Page (2014) confirmed that U.S. policy outcomes track elite preferences with near-zero responsiveness to median-income voters. When economic structures stop responding to democratic inputs, citizens disengage from democratic processes. U.S. midterm turnout has remained below 42% in all but one cycle since 2000.

What the models found.

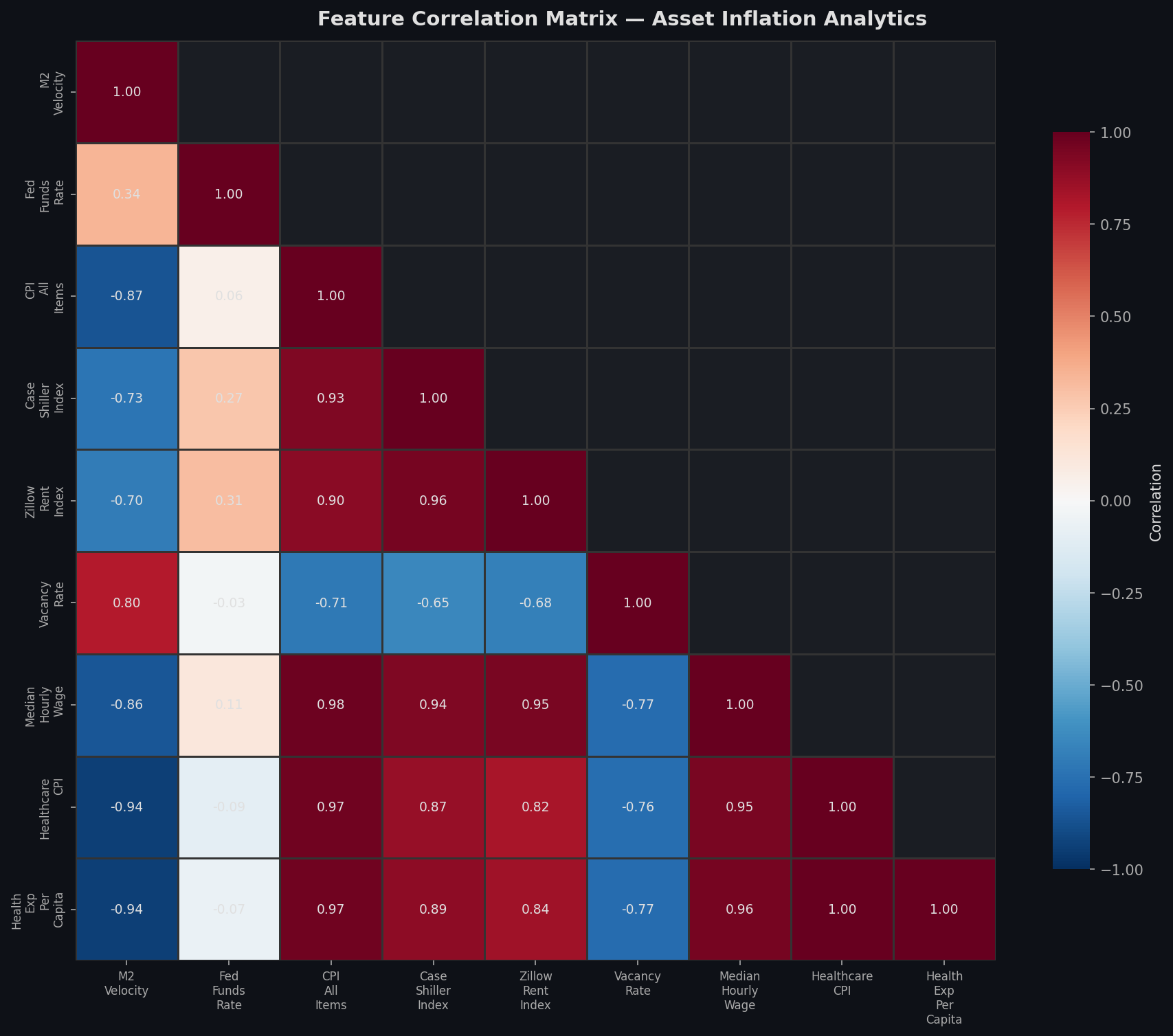

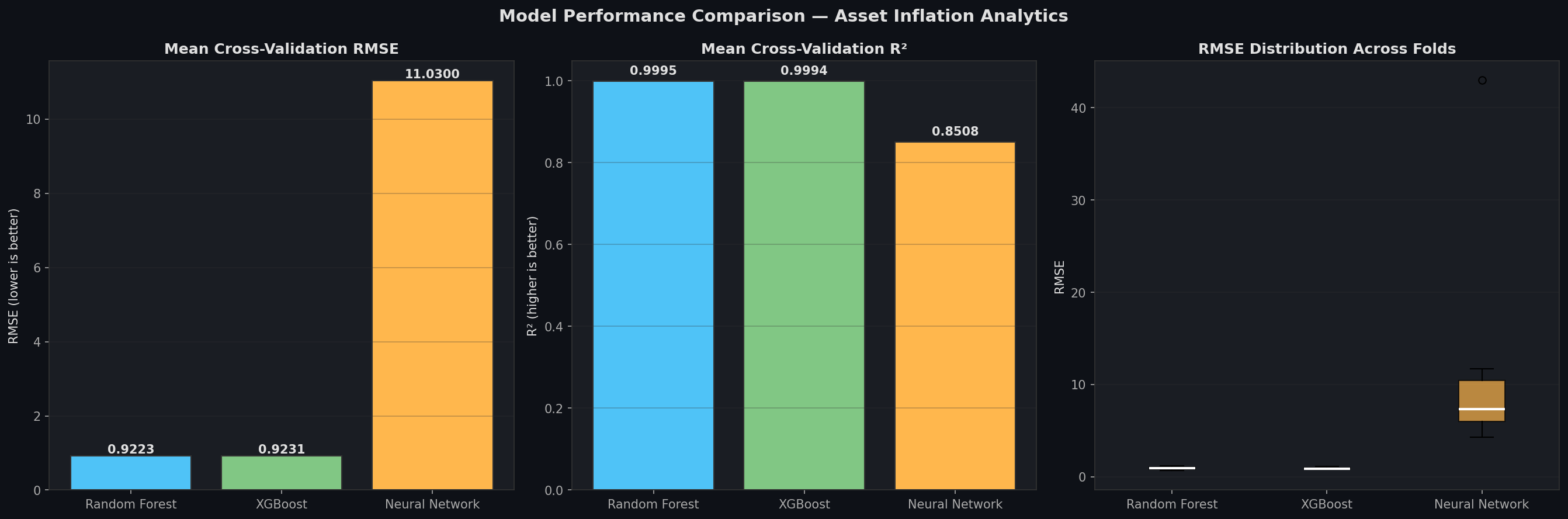

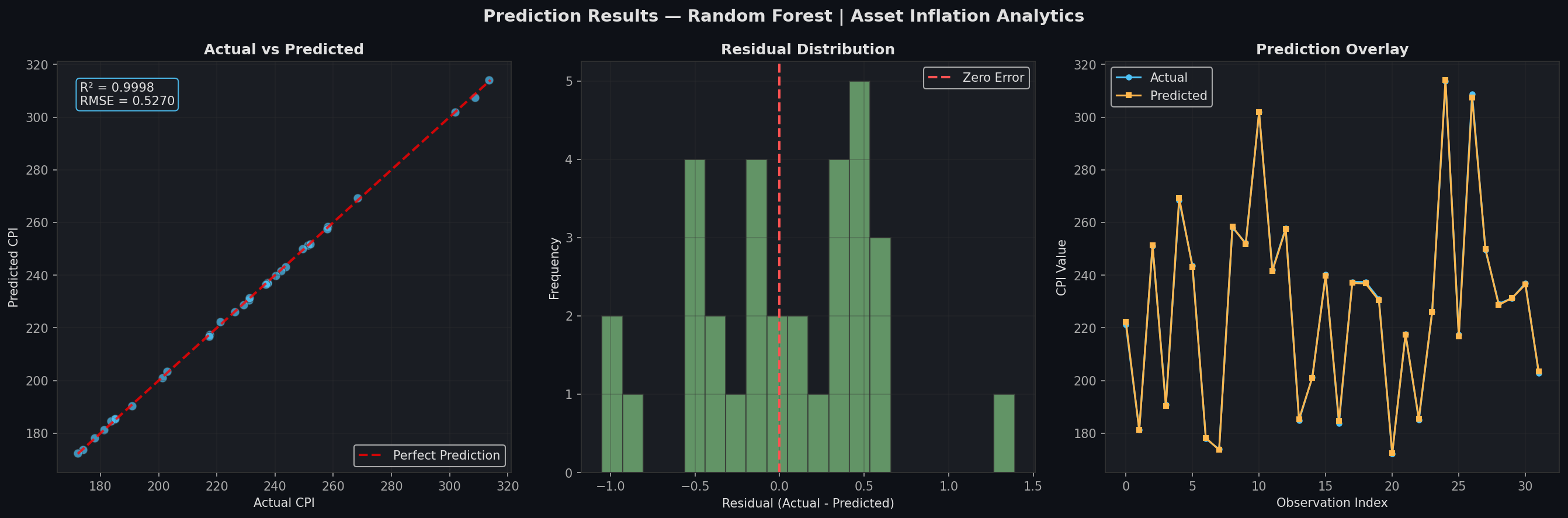

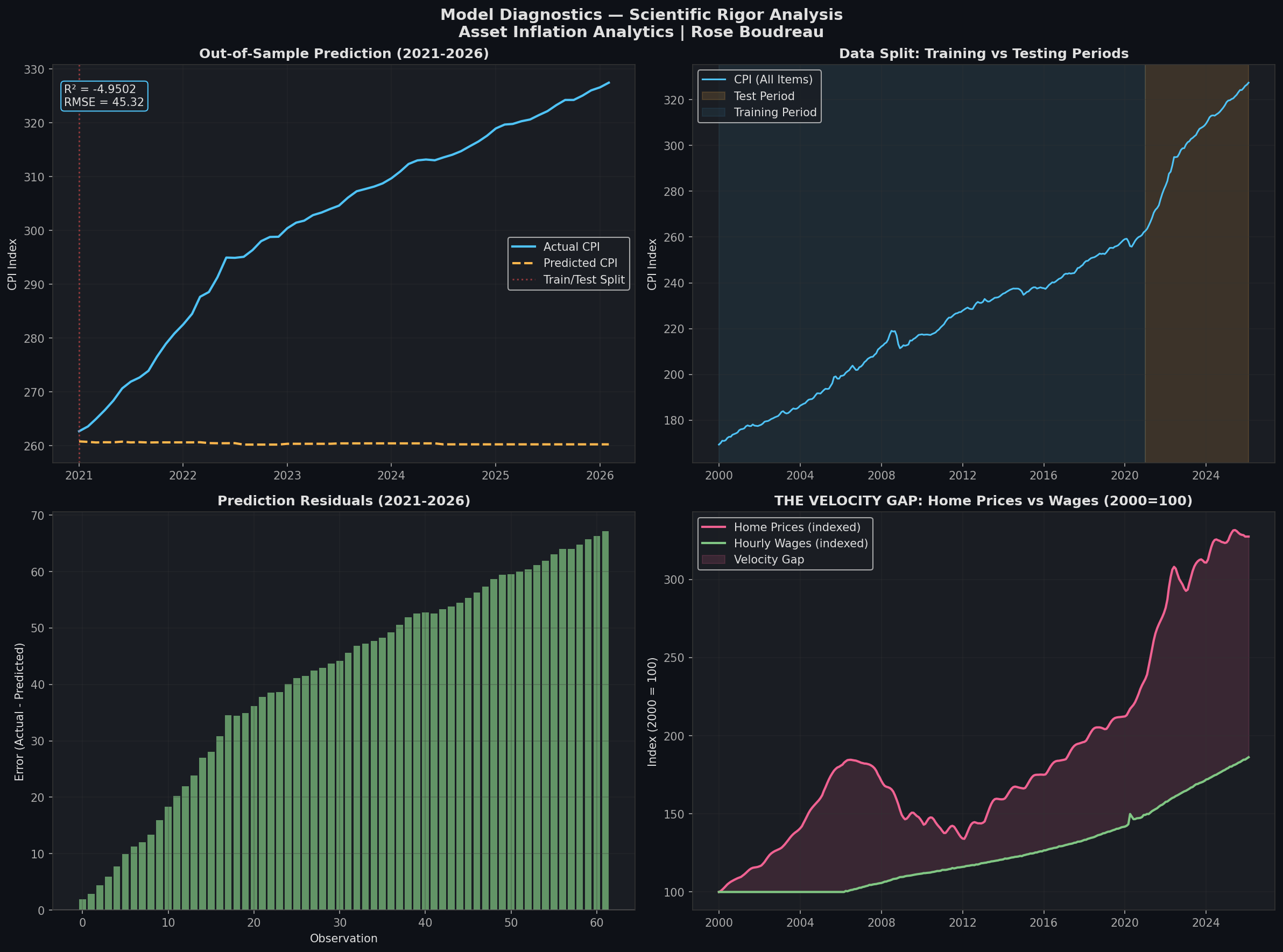

Three ML algorithms (Random Forest, XGBoost, Neural Network) were trained on 26 years of monthly data to predict CPI from housing, wage, and monetary indicators. In-sample R² reached 0.9995. That figure is inflated by multicollinearity: Healthcare CPI, wages, home prices, and health expenditure all trend upward together because they are products of the same economic system. The model restates the correlation matrix, not a hidden causal relationship.

The critical test was temporal validation. Trained on 2000 to 2020 and tested on 2021 to 2026, every model failed: R² dropped to -4.95. The Chow test (Chow, 1960) independently confirmed a structural break at the point of maximum divergence. The post-2020 economy is not a continuation of the pre-2020 regime. It operates under different parameters.

To address the multicollinearity concern directly, a first-differences model was run: predicting month-over-month CPI changes from month-over-month feature changes, with all shared trends removed. Granger causality tests (Granger, 1969) were applied to determine whether asset price changes temporally precede CPI changes. Both tests confirm a real signal beneath the trend-driven inflation of the level-based model.

The subsistence thesis.

The conventional expectation is correction: asset prices will moderate, wages will catch up, the gap will close. The data does not support this. The velocity ratio between asset growth and wage growth is accelerating, not oscillating. The M2 velocity decline is monotonic. Case and Deaton (2020) documented how the downstream effects of this shift manifest as "deaths of despair," concentrated in populations for whom economic mobility has been structurally foreclosed.

If wages cannot generate the surplus required to acquire assets, and asset ownership is the primary mechanism for wealth accumulation, then wages have been reduced to a subsistence function. Housing becomes a perpetual cost, not a savings vehicle. Healthcare becomes a debt instrument, not a service. The economy has shifted from a mobility regime to a subsistence regime, and the shift occurred so gradually that most people experienced it as individual failure rather than systemic redesign.

The structural break in 2020 formalized what had been building for two decades. The relationship between labor income and the cost of living changed. Not temporarily, and not in a way that historical patterns can predict. The institutions that govern housing, healthcare, and monetary policy are social constructs. They were built by decisions. The data presented here does not prescribe what should be done. It documents, with precision, what has already happened.